Summary of Regulation In Philippines

- REGULATOR

- REGULATED ENTITIES

- Banks

- Non-Bank Financial Institutions, when carrying out quasi-banking activities

- Non-stock Savings and Loan Associations

- Pawnshops

- Lending and Financing Companies

- Insurance and Reinsurance Companies

- Mutual Benefit Associations

- Cooperative

- Other Credit Granting Entities, if registered

- TYPES OF REGULATION

- Prudential regulation and non-prudential regulation for Banks and Non-Bank Financial Institutions

- Non-prudential regulation for other registered credit granting entities

- LIST OF TRUTH-IN-LENDING ACTS

Truth-in-lending Legislation in Philippines

Overview .

The truth-in-lending legislation in the Philippines was first enacted in 1963 through the Truth in Lending Act. The Act, and its implementing regulations and circulars (collectively, the “Act”), is not specific to the microfinance sector but applies to all loan agreements between most credit providing institutions and their borrowers. Notable exceptions include certain consumer Lenders, such as car dealers and appliance stores (although pawnshops are required to comply with the Act).

The Act requires certain minimum information disclosures to inform the borrower of the full terms and conditions of the loan. Best practices demonstrated by the Act include the prohibition on the Lender’s ability to charge “flat” interest rates, and a requirement for concise and complete disclosures.

The Central Bank of the Philippines, through its Monetary Board, issued Circular No. 730 for Bank entities in 2011, Circular No. 754 for Non-Bank Financial Institutions in 2012 and Circular No. 755 for Credit Granting Entities not covered by the above Circulars in 2012

Disclosure Requirement

The Act sets out guidelines for the minimum disclosure requirements from Lenders and the manner in which the total cost of credit must be computed and communicated to the borrower. The relevant loan agreement and other loan documentations are required to specify at least the following minimum loan conditions: the total amount to be financed; the finance charges associated with the loan; the net proceeds of the loan (reflecting all bank charges or deductions), and an effective annual interest rate, as described below.

The Act requires disclosure of the percentage that the finance charge in relation to the total amount financed, expressed in terms of either a simple annual rate or an effective annual interest rate, depending on the repayment method. Lenders are also obliged to display the information required in the disclosure statement in conspicuous places at their business premises.

Remedies and Enforcement Mechanism

The Act imposes criminal liability on Lenders who violate its provisions, and for a civil right of action for borrowers, which includes the right to recover up to twice the finance charges associated with the loan.

For more detailed aspects of the truth-in-lending directives in the Philippines, please download the Legal Summary Document referenced above.

National Truth-in-lending Formula

National Formula

Formula Description

Lenders governed by the Act are required to charge interest based only on the outstanding loan balance at the beginning of an interest period (i.e., charging “flat” interest is prohibited).

For installment loans (i.e., principal is payable in installments), interest per installment period shall be computed based on the outstanding balance of the loan at the beginning of each installment period. All loan documents are required to show repayment schedules in a manner consistent with this provision.

The Act provides two methods of annual percentage calculation, depending on the manner the principal balance is payable, as described below: .

- Simple Annual Rate – when the loan is payable in one year or less, with a single end payment upon maturity and there are no upfront deductions to principal, Lenders must calculate the simple annual interest rate, which represents the ratio between the finance charge and the amount to be financed.

- Effective Interest Rate – Lenders are required to employ the effective interest rate (EIR) method for all loan terms different from the simple annual rate assumptions noted above. Lenders may alternatively provide a monthly effective rate for loans, thus stating the contractual interest rates on a monthly basis.

As guidance to Lenders, the Circulars described above provide model illustrations for the EIR calculations of common loan features. Due to the limitation of the model’s ability to calculate the EIR for all possible transactions, the Circulars require that Lenders be responsible for the accuracy of their EIR calculation based on the actual features of the loan transactions.

Formula

The EIR is defined as the rate that exactly discounts estimated future cash flows through the life of the loan to the net amount of loan proceeds. For consistency, methodology and standards for discounted cash flow models are prescribed for this purpose. The Circulars do not prescribe a standardized national formula to calculate the EIR. However, they do provide excel-based model illustrations for common loan features.

The Circulars also outline the components of the finance charges that should be included in the EIR calculation. For a regular credit transaction these components are interest, fees, service charges, discounts, and such other charges incident to the extension of credit. For credit card transactions the components are interest, fees, service charge and such other charges incident to the extension of credit.

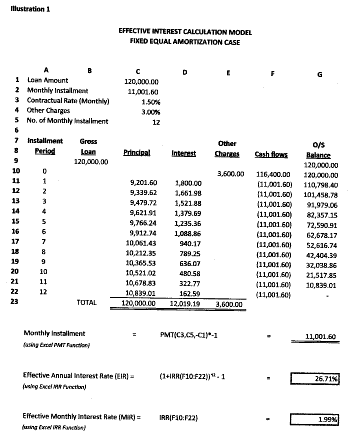

Please see below one of the model illustrations and the formula provided to calculate the EIR for a common loan feature. Please check the Circulars listed above for details of other loan scenarios

The model illustration above shows the calculation of the EIR for a fixed amortization case, employing the excel built-in PMT and IRR functions:

- For determination of monthly installment = PMT( Function) * -1

- For determination of effective annual interest rate (EIR) = (1+IRR(cash flow))^12 – 1

- For determination of effective monthly interest rate (MPR) = IRR(cash flow)

Pricing Components in the National Formula

Pricing Components Included

- Nominal interest rate

- Fees and service charges

- Other finance charges associated with the loan

- Mandatory credit Insurance

Pricing Component Excluded

- Compulsory deposit (Not Prohibited)

- Conditional charges (Not Prohibited)

- Penalty charges (Not Prohibited)

No Comments