Summary of Regulation In Ecuador

- REGULATORS

- REGULATED ENTITIES

- Banks

- Other Credit Granting Organizations

- TYPES OF REGULATION

- Prudential and non-prudential for Banks

- Non-prudential for other credit granting entities

- LIST OF TRUTH IN LENDING ACT

Truth-in-lending Legislation in Ecuador

Overview

.

The Central Bank of Ecuador, through its Board of Directors, is responsible for implementing, executing and applying the monetary, financial and credit policies in Ecuador.

.

The Central Bank introduced the first truth-in-lending regulation in 2007, the “2007 Regulation” and later consolidated this regulation with additional provisions in 2014, the “2014 Regulation,” collectively called the “Regulations.”

.

The Regulations apply to all Lender institutions that are part of the national financial system in Ecuador. These include Lenders involved in commercial, consumer, micro-credit and housing lending. In special circumstances, the Regulations also apply to financial transactions outside the national financial system.

.

Disclosure Requirement

.

The Regulations require Lenders to disclose details of all relevant loan terms and conditions, both prior to making a loan and upon the actual making of the loan. To assist in the uniform disclosure of pricing provisions by all Lenders, the Regulations provide a corresponding formula for calculating the effective annual interest rate (TEA) and the effective annual financing cost rate (TEACF), each as described below in more detail.

.

Lenders are required to provide an automatic credit simulator on their website, running at least the two basic amortization schedule options, allowing customers to simulate different amounts, terms and TEAs and providing the corresponding TEACF for each case.

.

Further, the Regulations also mandate that interest payable by a Borrower always be calculated on the balance of principal due, regardless of the amortization schedule selected.

.

When advertising for credit, Lenders are required to provide truthful information and specify the nominal interest rate and TEAs for each term, and the frequency of interest payments.

.

Remedies and Enforcement Mechanism

.

The Regulations do not create any specific remedies for Borrowers against Lenders. The Regulations provide that any failure by an institution to provide the Central Bank of Ecuador with the periodic required information shall be reported to the Banking and Insurance Superintendence so that it may impose the relevant sanctions under applicable law.

.

For more detailed aspects of the truth-in-lending directives in the Philippines, please download the Legal Summary Document referenced above.

National Truth-in-lending Formula

National Formula

Formula Description

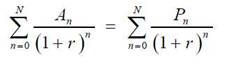

The TEA is calculated based on the internal rate of return associated with the cash flows under a credit extension. The TEACF, on the other hand, is calculated taking into account all the disbursements and payments made under a credit extension, including all costs (defined as any amounts directly related to the loan, which are paid by the Borrower to the Lender) and expenses (defined as any amounts indirectly related to the loan, which the Borrower must pay to third parties as a result of the loan, such as life insurance and taxes.

.

The Regulations require that Lenders calculate the TEA and TEACF taking into consideration the number of days between the extension of credit and its maturity.

.

Lenders are also required to charge a nominal interest rate within the maximum TEA limit set by the Regulator. The maximum TEAs are established on a rolling basis for each month, based on the calculation period, described in the Regulation.

Formula

The formula provided by the Regulations to calculate the TEA and TEACF is based on the internal rate of return formula, by which the present value of the disbursements made at period n equals the present value of loan repayments and expenses related to the loan, payable by the Borrower in each period n.

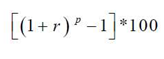

Mathematically, the TEACF is defined as:

.

.

.

Where r, is given by:

.

.

r = rate financing cost of period n;

p = frequency of payments of credit, expressed as number of payments in a year;

(e.g. Schedule of payments: monthly = 12; bimonthly = 6; quarterly = 4; semi-annually = 2 ….)

n = period of credit; 0 <n <N;

n = 0, a period in which the first disbursement is received;

n = N, a period in which the last payment is made;

An = disbursement actually received in period n (excluding any reserve); and

Pn = payment made in period n (including all expenses and costs related to credit).

Pricing Components in the National Formula

Pricing Components Included

- Nominal Interest rate

- Fees and Commissions

- Compulsory Deposit

- Insurance (expressly included in the Regulations in 2014)

- Taxes (expressly included in the Regulations in 2014)

Pricing Component Excluded

The Regulations do not expressly exclude any component from calculation of the formula.

No Comments