Microfinance Pricing Report: Uganda

Available Downloads

Languages available: EnglishThe Uganda Microfinance Pricing Report 2013 presents in-depth analysis of the prices paid by microfinance borrowers in Uganda. The report draws out key themes, features and trends in pricing, basing its analysis on prices calculated using original loan documentation representing real client loans in Tanzania. The report covers the loan products accessed by 418,185 of Uganda’s borrowers, representing 85% of the total market.

This analytical report was prepared by MFTransparency in partnership with Planet Rating and with funding from MasterCard Foundation. Further data collected via the Transparent Pricing Initiative can be seen, downloaded and interacted with on the Uganda pages of MFTransparency’s Pricing Data Platform.

Executive Summary

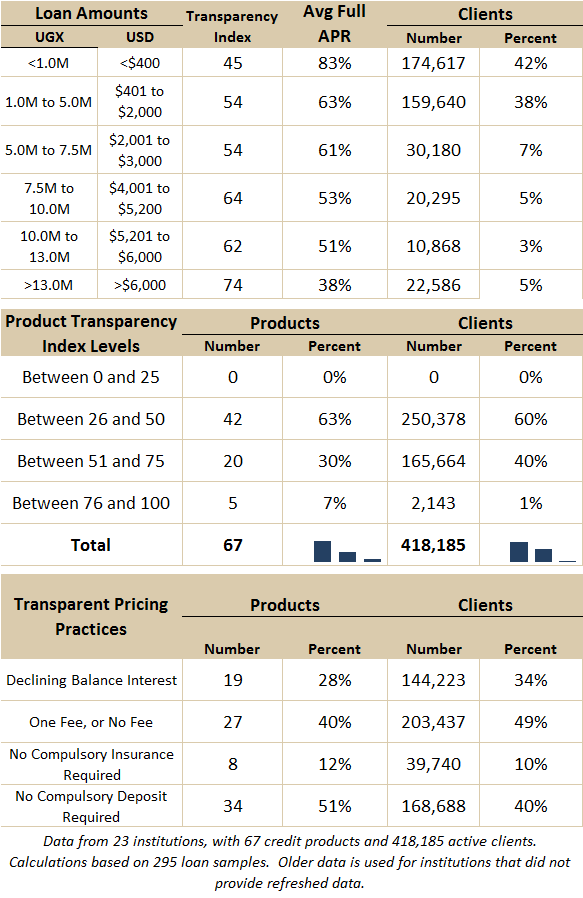

- The Pricing Transparency Index ranges from 30 to 90 in Uganda and averages 48, which is within regional benchmarks but still at a low level.

- Only a minority of borrowers benefit from loans priced transparently, with just 1% of borrowers receiving loans with a Transparency Index above 75/100.

- This low level of transparency is explained by pricing practices consisting of multiple price components: 66% of borrowers receive loans in which interest is calculated using a flat interest method; 98% of borrowers pay fees in addition to the interest rate; 60% of borrowers provide up-front compulsory deposits and 90% of borrowers pay a compulsory insurance fee. The few MFIs with a high Transparency Index use declining rates and a limited number of fees.

- Microfinance pricing data shows that the true prices increase as loan sizes get smaller. As those true prices rise, the interest rate communicated to the borrower becomes less indicative of the true price and therefore, the corresponding Transparency Index value decreases. Inversely, larger and longer term loans are priced more transparently. Cooperatives and Banks tend to be more transparent than other MFIs. The former often use simpler pricing mechanisms in Uganda (not always true in other countries). Some of the latter group have developed a strategy to offer cheaper and more transparent loan products than the market by subsidizing smaller loans with larger loans.

No Comments