Microfinance Pricing Report: Rwanda

The Rwanda Microfinance Pricing Report 2013 presents in-depth analysis of the prices paid by microfinance borrowers in Rwanda. The report draws out key themes, features and trends in pricing, basing its analysis on prices calculated using original loan documentation representing real client loans in Rwanda. The report covers the loan products accessed by 68,714 of Rwanda’s borrowers, representing 92% of the total market.

This analytical report was prepared by MFTransparency in partnership with Planet Rating and with funding from MasterCard Foundation. Further data collected via the Transparent Pricing Initiative can be seen, downloaded and interacted with on the Rwanda pages of MFTransparency’s Pricing Data Platform.

Executive Summary

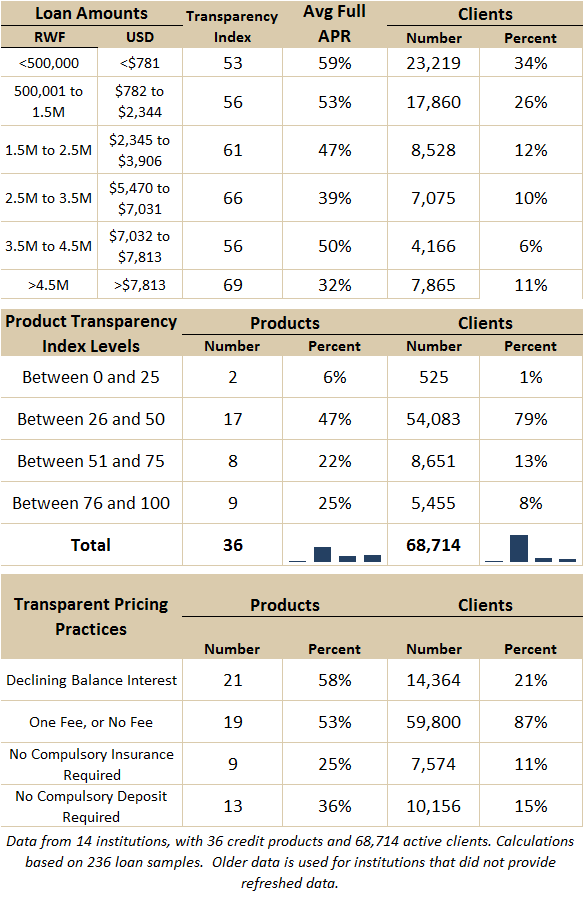

- The institutional level Pricing Transparency Index ranges from 40 to 71 in Rwanda and averages 52, which is within regional benchmarks but still at a low level.

- Few clients benefit from loans priced transparently as only 14% of them receive loans in which the Transparency Index is above 75/100.

- This low level of price transparency is explained by the use of multiple price components: 51% of borrowers receive loans which use a flat interest rate calculation method; all borrowers pay fees in addition to the interest rate; 55% provide up-front compulsory deposits while 34% provide on-going compulsory deposits. In addition, 55% of borrowers pay a compulsory insurance fee.

- There is a strong association between a loan product’s price and its level of pricing transparency: as Full APR increases, the corresponding Transparency Index value decreases. Expensive loans tend to lack transparency in communicating the true price paid by the borrower. This is notably due to the frequent use of flat interest rates for small loan amounts.

- Data indicates that the Full APR increases dramatically for shorter-term loans and for smaller loans. However, on-going compulsory deposits contribute to increasing the price as the duration of the loan increases.

- Cooperatives are more transparent than other institutions, notably due to the use of declining rates. Their average Full APR is also lower, in part because they may access cheaper funding through deposits mobilization.

No Comments